Quadrise Plc (LON:QED) has developed emulsion fuel technology products which we believe have a key role to play in the global energy transition. Unlike many energy transition solutions, we see their products as minimising disruption while achieving significant environmental gains. Targeting high-emission energy sectors like shipping, heavy industry, and power; QED offers stable and safe fuels and biofuels without expensive upgrades. Their development pipeline includes zero carbon fuels, aligning with steadily tightening legislation. The current products are all based on the company’s oil-in-water emulsion technology, and this approach differentiates QED from competitors that produce water-in-oil emulsion fuels, while the management team has previously successfully commercialised an oil-in-water product with the Venezuelan state oil company.

Near-Term Commercialisation

The company has three advanced commercial trials underway, each of which if translated into a full commercial agreement, would have a transformational impact on the earnings and valuation outlook. The company has two business models: the licensing and tolling of its emulsion fuel products. We anticipate that the licensing model could deliver annual EBITDA of around US$8-9mpa while tolling could deliver between US$15-22mpa each, with just four manufacturing units installed. Over a ten-year timeframe, these contracts would deliver pre-tax NPV8 of US$45-90m respectively, depending on the product and target sector. The recent signature of the Utah based project agreement could bring commercial revenue as soon as August 2023 while upcoming talks are expected to lead to an agreement in Morocco with an industrial group in H2 2023 while testing for the marine project is due to commence on the marine project in Q4 2023.

Recommendation

The company recently announced that it has raised £1.94m by way of an accelerated book build and open offer. Management believes this will provide sufficient working capital to successfully complete the current three commercial trials, secure commercial agreements and revenues thereafter.

Although we have presented scenario analysis and the potential impact of commercial success, we do not yet have sufficient visibility for full forecasts and a quantitative valuation. That said, trading at close to all-time lows but with multiple advanced commercial trials, the risk reward on offer currently is attractive particularly given the status of these trials and now that the company has strengthened its balance sheet.

Investment Case Summary

QED presents an attractive investment opportunity, with two saleable products already in the market and one in development. The progression from MSAR to bioMSAR, along with the upcoming bioMSAR zero, offers a viable pathway for companies heavily reliant on fossil fuels to gradually decarbonise their energy use. This aligns with increasingly stringent legislation concerning air quality and carbon emissions. QED’s proprietary emulsion technology allows businesses to achieve this transition without incurring the high capital investment typically associated with alternative transitional energy technologies.

QED’s products demonstrably and quantifiably improve fuel efficiency through total combustion, thereby reducing nitrous oxide (NOx) emissions and soot (particulate emissions). bioMSAR which uses glycerine, builds on this by delivering a significant reduction (up to 25%) in carbon dioxide (CO2) emissions making it comparable to natural gas, which for many industries is the obvious transition fuel despite the high cost required to retrofit engines or supply LNG.

The Journey from MSAR to bioMSAR to bioMSAR Zero

SOURCE: Company Data, VSA Capital Research.

With emissions legislation tightening progressively over the next decade, beyond the reduction that LNG offers against HFO, LNG is likely only an interim option. QED’s pipeline which includes a net zero biofuel will build on the existing principles of compliance with conventional engines. In an uncertain and rapidly changing landscape, this flexible option that avoids intensive investment is expected to be an attractive selling point to customers. Recent developments such as the EU’s softened position on efuels, highlight the challenges faced by the industry and suggest further changes ahead.

For the Mediterranean Shipping Company (MSC), with whom QED is progressing towards commercial agreement, we estimate that with a fleet of over 800 ships the cost to retrofit to LNG could range from US$16-25bn with the estimated cost per ship at between US$20-30m. Around US$500m (US$625k per ship) in investment into QED equipment would provide sufficient capacity for 100% of the current fleet. QED fuels are expected to save MSC 10% on fuel bills totalling some US$5bn annually (assuming 10mntpa fuel is used by MSC at US$500/t on average today). Given that further investment into an alternative other than LNG will likely be required within the next twenty years, QED products appear an attractive and less disruptive alternative.

QED has commenced three key projects which are at an advanced stage, all of which could lead to commercial agreements within the next twelve months. These are in the key target industries with prominent industry groups in the marine, industrial and upstream oil sectors.

The Utah Oil Sands project with Valkor Technologies is the most advanced and with the recent announcement of a Site License and Supply Agreement, the company could begin to receive commercial revenues as soon as August 2023 on the back of well permitting, where a hearing date has been set with the authorities in Utah. Although conditional this would be a major milestone for QED triggering initial staged payments of up to US$1.5m.

Prior to the commercial agreements themselves, we expect interim milestones arising from the successful completion of testing. Aside from Valkor, the first of these is likely to be the completion of testing in Morocco where the QED systems and fuels are onsite, although we note an equipment failure has temporarily delayed testing whilst a replacement is installed.

Obtaining a Letter of No Objection (LONO) from Wärtsilä for bioMSAR in relation to the MSC trial is another potential catalyst as this not only demonstrates the success of this individual trial but that the company are satisfied that QED products can be used on their engines as MSAR has already received an interim LONO. Wärtsilä is one of the shipping industry’s largest engine manufacturers globally, almost two hundred years old with a market capitalisation of US$7.6bn and while positive testing results have previously been published, the LONO would be a significant validation and derisking milestone for QED that could be used in seeking commercial agreements more widely for their fuels.

Near-Term Opportunities

| Project | Stage | Next Steps |

|---|---|---|

| Morocco Industrial Group | Commercial testing underway | Fuel Supply Agreement Q3 2023 |

| Mediterranean Shipping Company | Refit of demo ship underway in dry dock | Three-way agreement with QED, MSC and a fuel supplier for the trial. |

| Utah Oil Sands (Valkor) | Drilling permits outstanding due August 2023 | Signature of licence agreement with Valkor, subject to award of permits. |

Investment Summary

The company recently announced that it had raised a total of £1.94m at 1.25p/sh. by way of an accelerated book build and an open offer. The proceeds are used primarily for working capital and the completion of the commercial trials. This should therefore take the group through to commercial revenue providing working capital into calendar H2 2024.

In the context of the groups QED is speaking to, a successful agreement with any or each would be transformational, and our analysis based on just four MMUs represents only a small proportion of these groups’ total consumption of substitutable fuel.

Although the commercial testing is approaching a crucial time, commercial agreements are to be agreed on completion of the testing and at this stage it is not possible for us to determine group forecasts with conviction. Our analysis is based on management guidance of how licensing or tolling agreements are likely to look demonstrating that the installation of four MSAR Manufacturing Units (MMUs) that would power 45 ships or provide 0.9mntpa of fuel oil could generate revenue to QED of US$26-57m and EBITDA of US$6-14m.

Target Markets

Since Covid 19, the rationale for decarbonisation and the transition to Net Zero has been accelerated, enshrined in legislation with financial and practical implications for companies and industries which do not adapt their operating practices to suit the proposed changes.

QED’s technology and suite of products provide an opportunity for some of the most intense Greenhouse Gas (GHGs) emitters such as shipping, industrials, cement manufacture, and power generation to progressively decarbonise without major upfront investment. QED’s products with minor adaptation work well with existing boilers and engines and the company’s current commercial trials reflect the breadth and depth of opportunity.

Marine

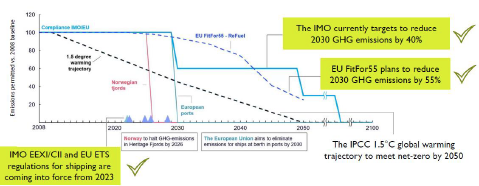

The marine industry is responsible for transporting 90% of world commerce and is almost entirely powered by heavy fuel oil (HFO) consuming in excess of 300mntpa, making the industry one of the most significant contributors to global GHGs. As a result, the International Maritime Organisation (IMO) has set a target to reduce CO2 emissions from the industry by 40% by 2030 and 70% by 2050.

A number of measures are being introduced by the IMO such as the Energy Efficient Design Index, Energy Efficiency Existing Ship Index, the Carbon Intensity Indicator, and the Ship Energy Efficiency Management Plan to monitor these efforts which coincide by regional legislative changes such as by the EU including the Emissions Trading system Directive which now encompasses the maritime sector. The FuelEU Maritime Regulation comes into effect in 2025 and is more aggressive than the IMO targets requiring a 2% reduction in GHG intensity by 2025 against 2020 and 75% by 2050 with intermediate targets to that point. Shipping companies that fail to comply will be fined and may eventually be banned from EU waters.

LNG is around 25% less emissive than conventional marine fuel in relation to CO2 and is often cited as an option for the industry to reduce emissions. It is considered a transitional fuel by the EU and is comparable to the performance of bioMSAR in this respect; however, retrofitting a ship to run on LNG can cost at least US$20m. Across a fleet this would be a substantial cost and would only be a temporary solution. Furthermore, when emissions are measured on a full life cycle basis (e.g., “well-to-wake”) the 25% reduction (measured on a “tank-to-wake” basis) from LNG becomes significantly lower, and potentially zero if methane slip occurs in the production and supply chain.

Each of QED’s production units costs an estimated US$7m to install and can provide fuel for around 12 ships, while the development pipeline which uses substantially the same production technology includes a net zero biofuel which would likely align with the longer-term standards required of the industry.

New Regulations are Driving the Requirement to Decarbonise

Heavy Industry

Schemes such as the EU Emissions Trading Directive affect all heavy industry not simply the maritime industry. The cap-and-trade approach means that the base of available credits reduces each year, implying the cost of emitting carbon should increase over time. Consequently, heavy industry such as cement manufacturing or non-renewable power is incentivised to decarbonise wherever possible. Cement accounts for 7% of global carbon dioxide emissions with fossil fuels burned to generate the heat required to produce cement clinker.

The incentives for changing are not simply the efficiency savings but reducing the impact of financial penalties of non-compliance. With QED’s pipeline of products including a net zero bioMSAR moving to the current product range, it is a transitional step that avoids intensive spending on new infrastructure. The company’s commercial trials in Morocco and Utah represent significant opportunities for traction within this space.

To continue reading this report please see or download the Quadrise VSA Capital PDF: