Kingfisher plc (LON:KGF) has announced its final results for the year ended 31 January 2023.

Highlights

· A year of solid execution

– FY performance in line with our expectations & guidance, against strong prior year comparatives

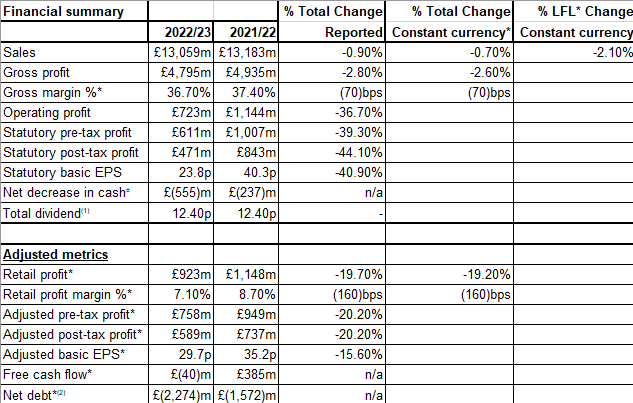

– Total sales -0.7% in constant currency and LFL -2.1% (3-year LFL* +15.6%)

– Sales outperforming home improvement industry growth, with 3-year total sales CAGR(3) of +5.9% vs market CAGR(4) of +4.9%

– Total e-commerce sales* -9.1% (3-year growth +146%), with growth of +3.7% in H2. E-commerce sales penetration* of 16.3% (FY 19/20: 7.9%)

– Adjusted pre-tax profit (PBT) -20% to £758m (+39% vs FY 19/20). Statutory PBT -39.3% to £611m

– Exceeded target for 1.5°C science-based scope 1 and 2 carbon reduction (-52.7% vs FY 16/17)

– Proposed total dividend maintained at 12.40p per share, in line with FY 21/22

· Multiple profitable growth opportunities being pursued at pace

– Ambition of 25% e-commerce sales penetration. Successful e-commerce marketplace launches in the UK and Iberia*; preparing roll-out in Poland and France*

– Opened first 5 Screwfix stores in France; up to 25 new stores planned in FY 23/24

– Record 82 Screwfix store openings in the UK & Ireland*; up to 60 new stores planned in FY 23/24

– Targeting up to 80 medium-box and compact store openings in Castorama Poland over 5 years

– Continued focus on increasing trade penetration across all banners. TradePoint (in B&Q) 3-year LFL sales growth of +31.5%, outperforming core B&Q and reaching 22% sales penetration

· Well positioned to navigate FY 23/24

– Resilient underlying sales trends in the new year (February 23/24 LFL sales(5): +0.5%)

– Maintaining strong price indices in our key markets, and continuing to deliver value to customers

– Own exclusive brands (45% of sales) providing customer benefits and support to gross margin %

– Effectively managing inflation, costs and inventory levels

– Comfortable with current consensus of sell-side analyst estimates for FY 23/24 adjusted pre-tax profit(4), with expectation of >£500m free cash flow for the year

· Announcing new medium-term financial priorities; confident in growth and cash generation opportunity

Thierry Garnier, Chief Executive Officer, said:

“Across all our markets, sales have remained resilient in both DIY and DIFM/trade channels, with like-for-like sales 15.6% ahead of pre-pandemic levels. We have maintained a sharp focus on pricing to deliver value to our customers during this challenging period for household finances, while at the same time managing our cost inflation pressures effectively. Strong supply chain management has ensured good product availability and a firm grip on our inventories.

“We continue to execute our strategy at pace and invest in our multiple growth opportunities. We are proud of the progress our teams have made during the year, and since the start of our ‘Powered by Kingfisher’ strategy. Our e-commerce sales have increased by 146% over the last three years and we have enhanced our online proposition with the launch of marketplace offerings in the UK, Spain and Portugal, which are all performing strongly. Across the Group, we are strengthening our proposition for trade customers, building on the success of B&Q’s TradePoint and the accelerated expansion of Screwfix. Whilst it’s still early days for Screwfix’s ambitions in France, we are happy with the results of the first few months of operations and planning for up to 25 more store openings this year. We are also building on our leadership position in Poland and the attractive potential of this market by opening seven more Castorama stores in 2023.

“We remain confident in both the growth of our industry, and in our strategic priorities supporting growth ahead of our markets. And we are announcing today our new medium-term financial priorities, focused on growth, cash generation and higher returns to shareholders.”

FY 22/23 Group results

· Sales down 0.7% in constant currency, reflecting strong prior year comparatives linked to high demand for home improvement products. Resilient sales across both retail and trade channels

· LFL sales down 2.1% and corresponding 3-year LFL up 15.6%

– Double-digit 3-year LFL sales growth across all banners

– Positive 1-year growth in Poland, Iberia and Romania; resilient performance in France; strong prior year comparatives for the UK & Ireland

· Q4 22/23 LFL sales flat, and up 13.7% on a 3-year basis, broadly consistent with the trend from Q3 22/23 (LFL +0.2%; 3-year LFL +15.3%)

· Gross margin % down 70 basis points to 36.7% (FY 21/22: 37.4%; FY 19/20: 37.0%), reflecting banner & category mix, and the impact in H1 of ‘normalised’ promotional activity and one-off logistics spend to secure/manage seasonal and ‘buffer’ stock

· Retail profit down 19.2% in constant currency to £923m (FY 21/22: £1,148m; FY 19/20: £786m), largely reflecting very strong prior year comparatives in the UK & Ireland and France

· Statutory pre-tax profit down 39.3% to £611m (FY 21/22: £1,007m; FY 19/20: £103m), reflecting lower operating profit, including the impact of impairments following significant increases in discount rates and revised future projections

· Adjusted pre-tax profit down 20.2% to £758m (FY 21/22: £949m; FY 19/20: £544m), reflecting lower retail profit, partially offset by lower finance costs

· Free cash flow of £(40)m, down £425m (FY 21/22: £385m; FY 19/20: £191m), reflecting lower EBITDA* and one-off working capital outflow from completion of inventory rebuild programme

· Net decrease in cash of £555m (FY 21/22: £237m), largely reflecting lower free cash flow, and £583m of outflows in relation to ordinary dividends and share buybacks

· Net debt up to £2,274m (31 January 2022: £1,572m), including £2,444m of lease liabilities under IFRS 16, reflecting the net decrease in cash. Net debt to EBITDA of 1.6x (31 January 2022: 1.0x)

· Total dividend per share proposed of 12.40p (FY 21/22: 12.40p)

Outlook for FY 23/24

· Current trading:

– February 23/24 total sales +1.9% (LFL sales +0.5%)(5)

– Underlying sales trends remain resilient, with ‘big-ticket’ sales broadly flat YoY

– Expect some impact in March from adverse weather conditions and strong comparative in Poland

· Well positioned to navigate FY 23/24:

– Targeting further market share growth

– Sales impact of c.+1.5% from net space growth, largely from Screwfix and Castorama Poland

– Committed to active and responsive management of operating costs* to partially offset higher staff, technology and energy costs YoY

– Expect P&L investment of c.£40m in relation to our new businesses, including Screwfix France

· Based on the above, we are comfortable with the current consensus of sell-side analyst estimates for FY 23/24 adjusted pre-tax profit(6)

· Expect >£500m free cash flow for the year, supported by the unwind of working capital outflows in the prior year

· Intention to announce a new share buyback programme following completion of the existing programme this year; subject to our capital allocation framework and market conditions

Medium-term financial and capital allocation priorities

· Kingfisher operates in attractive markets, with new positive longer-term trends (such as more working from home and energy efficiency renovations) providing further support to market growth potential

· Financial priorities: Building on our industry’s attractive growth profile, the Group’s medium-term financial priorities are:

– Sales to grow ahead of our markets:

§ LFL sales growth driven by our strategic focus areas including e-commerce and marketplace, OEB, trade penetration; and

§ Sales impact of c.+1.5% to +2.5% from annual net space growth over the medium term, primarily driven by Screwfix and Castorama Poland

– Adjusted pre-tax profit to grow faster than sales:

§ Supported by scale benefits, higher margin initiatives, operating cost leverage, and multi-year operating cost reduction opportunities

– Strong cash generation to drive growth investment and shareholder returns:

§ Free cash flow of c.£400m to £500m in FY 24/25, followed by >£500m per annum from FY 25/26, supported by profit growth and ongoing inventory self-help measures

· Capital allocation: Our capital allocation priorities are as follows:

– Organic and ‘bolt-on’ inorganic growth opportunities that accelerate our strategy. Target gross capex of c.3.0-3.5% of total sales per annum, on average, focussed on delivering against attractive organic growth opportunities

– Maintain an efficient capital structure, with a more prudent position in times of macroeconomic uncertainty; maximum net leverage (net debt to EBITDA) of 2.0x over medium term

– Progressive, sustainable dividend policy, with target dividend cover* of 2.25-2.75x

– Surplus capital to be returned via share buybacks or special dividends

Executing strongly against our strategic priorities

· Grow by building on our different banners:

– Record 82 Screwfix store openings in the UK & Ireland for a total of 872 stores; up to 60 new stores planned in FY 23/24

– First 5 Screwfix stores opened in France; up to 25 new stores planned in FY 23/24

– 7 new Castorama stores opened in Poland; targeting up to 80 medium-box and compact store openings in Poland over the next 5 years

– First two B&Q franchise stores in the Middle East have opened

· Accelerate e-commerce through speed and choice:

– E-commerce sales penetration of 16.3%, twice the level of FY 19/20. Ambition of 25% sales penetration

– 91% of all e-commerce orders picked in store

– More options for click & collect (C&C) through roll-out of lockers in Poland; being tested at B&Q

– Adopting more last-mile delivery options, including successful roll-out of one-hour delivery (Screwfix Sprint) and optimised carrier management (being tested at B&Q and in France)

– Improved e-commerce order management through use of ‘digital hub’ stores and better visibility of available SKUs*

– New e-commerce marketplace model successfully launched at B&Q, Spain and Portugal (reaching 24% marketplace participation* at B&Q in February 2023, after just 11 months); preparing roll-out of marketplaces in Poland and France

· Build a data-led customer experience:

– Established ‘Centre of Excellence’ in data at Kingfisher with expertise in artificial intelligence (AI), machine learning, advanced analytics and data platform engineering

– New Group-developed recommendation engine implemented at B&Q and Screwfix, driving higher click-through and add-to-basket rates as well as faster response times

– Signed partnership with Google Cloud for infrastructure, platform services and AI solutions

– Utilising data analytics and AI to develop tools to support better pricing decisions, better promotional and markdown effectiveness, and enhanced visibility of our end-to-end supply chain

– Developing opportunities to quickly monetise our data capabilities through retail media, including advertising placed within our e-commerce platforms and apps

· Differentiate and win through own exclusive brands (OEB):

– OEB continuing to drive affordability, product innovation and reduced environmental impact, and carrying a higher gross margin % on average than branded products

– Total OEB product sales of £5.8bn, up 15.4% on a 3-year LFL basis and representing 45% of Group sales (FY 21/22: 45%)

– Good performance in kitchen, bathroom & storage and EPHC (electricals, plumbing, heating & cooling) categories, all showing YoY growth. All categories up on a 3-year LFL basis

– Completed roll-out of 32 new and redeveloped OEB brands to drive differentiation between retail banners and support extended ranges

· Develop our trade business:

– Accelerated Screwfix openings in the UK & Ireland, and strong progress in developing the proposition in France

– TradePoint (in B&Q) 3-year LFL sales growth of +31.5%, outperforming core B&Q and reaching 22% sales penetration (FY 21/22: 20%)

– Opened 18 new TradePoint counters in the UK and first 8 counters in Ireland

– Launched plan to grow trade customer penetration across all other banners, including new trade loyalty programmes in Poland and Iberia, and the introduction of new trade-focused services and OEB & branded product ranges

· Roll out compact store formats:

– Accelerated compact store tests; opened 17 new compact stores in the UK, France and Poland

– High street concept tests (B&Q Local in the UK, Casto in France and Castorama Express in Poland) continue to deliver encouraging learnings and results

– Small retail park concepts also showing positive results

– Entering final testing phase for Screwfix ultra-compact ‘XSR’ store format

– Planning to launch first test of a new Brico Dépôt France 1,000 sqm format in FY 23/24

· Lead the industry in Responsible Business and energy efficiency:

– Brought forward pay awards and support for colleagues to help manage higher costs of living

– Exceeded target for 1.5°C aligned science-based scope 1 and 2 carbon reduction, reducing emissions by 52.7% against a FY 16/17 base year

– Announced new net-zero emissions target for our operations (scope 1 and 2) by the end of 2040

– Sustainable Home Products (SHP) sales of £6.2bn, representing 47% of Group sales (FY 21/22: 44%). Raised target for growth of SHP to 60% by FY 25/26

– 11% of Group sales from energy and water-saving products

– Developed innovative end-to-end solutions at B&Q, Castorama France and Brico Dépôt France to help customers create personalised energy efficiency action plans for their homes, including access to relevant products and services

· Human, agile and lean:

– Embedding ‘test and learn’ culture across the Group, alongside key leadership behaviours to support delivery of our strategy

– Strengthened talent and capability in key areas, including technology, data and trade

– Multi-year cost reduction programmes continue to help offset inflationary pressures

– Four further store rightsizings completed in the UK, with improved sales densities at all locations

– Increase in net inventory YoY driven by inflation; inventory in units (volume) down

– Stock provisioning and de-listed stock rates remain below pre-pandemic levels

– Actions underway to further optimise supply chain, inventory management and sourcing footprint

Footnotes

(1) The Board has proposed a final dividend per share of 8.60p (FY 21/22 final dividend: 8.60p), resulting in a proposed total dividend per share of 12.40p in respect of FY 22/23 (FY 21/22: 12.40p). The final dividend is subject to the approval of shareholders at the Annual General Meeting on 27 June 2023.

(2) Net debt includes £2,444m lease liabilities under IFRS 16 in FY 22/23 (FY 21/22: £2,376m).

(3) Represents the compound annual growth rate (CAGR) of total sales for the UK, France and Poland between FY 19/20 and FY 22/23 (in constant currency).

(4) Market growth (in constant currency) for the UK, France and Poland based on a Kingfisher internal analysis covering 2,225 retailers (on a calendar year basis).

(5) February 23/24 total and LFL sales represents the calendar month February 2023 compared against February 2022, in constant currency. The figures are provisional.

(6) Guidance assumes current exchange rates. According to Company-compiled consensus estimates as of 14 March 2023, the current consensus of sell-side analyst expectations for FY 23/24 adjusted pre-tax profit is £633m.

Non-GAAP measures and other terms

Throughout this release ‘*’ indicates the first instance of a term defined and explained in the Glossary (Section 6). Not all the figures and ratios used are readily available from the unaudited final results included in part 2 of this announcement. Management believes that these non-GAAP measures (or ‘Alternative Performance Measures’), including adjusted profit measures, constant currency and like-for-like (LFL) sales growth, are useful and necessary to assist the understanding of the Group’s results. Where required, a reconciliation to statutory amounts is set out in the Financial Review (Section 5).

Final results announcement and data tables

This announcement and data tables for FY 22/23 can be downloaded from the Investors section of our website at www.kingfisher.com/investors. You can follow us on LinkedIn and Twitter (@kingfisherplc) with the results tag #KingfisherResults.

Results presentation

We will host an in-person results presentation for pre-registered analysts and investors today at 09.00 (UK time) at the London Stock Exchange, 10 Paternoster Square, London, EC4M 7LS. A simultaneous live video webcast of the presentation and Q&A will also be available via the Investors section of our website at www.kingfisher.com, and subsequently available on demand.