JPMorgan Japan Small Cap Growth & Income PLC (LON:JSGI) has announced its unaudited half year results for the six months ended 30 September 2021.

CHAIRMAN’S STATEMENT

Dear Shareholders,

Investment Performance

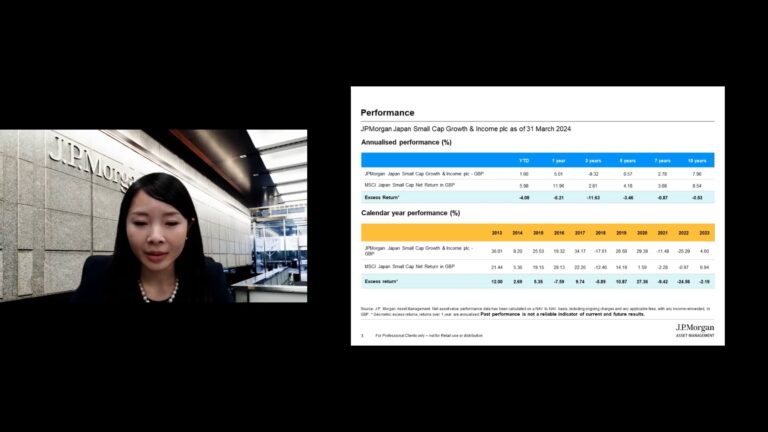

The first half of the Company’s financial year saw an improvement in Japan’s economic outlook, despite disappointment that the Tokyo Olympics had to be held without spectators. The vaccine roll-out gathered pace, the state of emergency was lifted at the end of September and survey data suggests manufacturing and service sector activity is increasing. Against this brighter backdrop, I am pleased to report that the total return on the Company’s net assets was +7.2% (in GBP) over the review period, compared to a total return of +4.9% for the benchmark, the MSCI Japan Small Cap Index. This amounts to an outperformance of 2.3 percentage points. The return to shareholders was higher, at +9.1%, reflecting a continued narrowing of the Company’s share price discount to its Net Asset Value (NAV).

The Company’s investment performance is explained in depth in the Investment Managers’ Report, along with details of recent portfolio activity. The managers also outline the themes they expect will drive Japan’s equity markets over the short term and beyond, and the reasons for their optimism about the Company’s long term prospects.

The Company continues to build on its strong long-term performance, as illustrated in the Financial Highlights, on page 4 of the Half Year Report and Financial Statements.

Dividend Policy and Discount Management

The Company’s revised dividend policy has now been in place for over three years. As a reminder, the dividend policy aims to pay, in the absence of unforeseen circumstances, a regular dividend equal to 1% of the Company’s NAV on the last business day of the preceding financial quarter, being the end of March, June, September and December. Over the year, this would approximate to 4% of the average NAV. This dividend is paid from a combination of revenue, capital and other reserves.

For the year ended 31st March 2021, dividends paid totalled 21.9 pence (2020: 17.7 pence). For this half year, two dividends of 5.5 pence and 5.8 pence respectively have been declared. Two further dividends will be declared on the first business day after 31st December 2021 and 31st March 2022.

One of the objectives of the revised dividend policy is to enhance the Company’s appeal to a broader range of investors. Since its introduction, it has therefore been pleasing to note some narrowing of the Company’s discount, driven by new demand, positive absolute and relative performance and favourable press commentary. Over the review period, the Company’s discount tightened from 8.7% to 7.2%, extending the recent narrowing trend. The Company did not repurchase any shares during the six months. However, the Board continues to monitor the discount closely and is prepared to repurchase shares to narrow the discount, when it feels this is appropriate, taking account of market conditions. At the time of writing, the discount is 8.3%.

Company Name and Ticker

Reflecting the now established dividend policy, the Company has changed its name to JPMorgan Japan Small Cap Growth & Income plc. This change took effect from 16th December 2020. Following the change of name, the Company also changed its London Stock Exchange stock ticker symbol (TIDM) from JPS to JSGI, with effect from 17th December 2020. The Company’s ISIN, SEDOL and LEI remain unchanged and it website URL was renamed www.jpmjapansmallcapgrowthandincome.co.uk.

Benchmark Index

Following a review of the composition of relevant indices, the Board changed the Company’s benchmark from the S&P Japan SmallCap Net Return Index (in GBP terms) to the MSCI Japan Small Cap Index (in GBP terms). This decision was reported in last year’s half year results and took effect from 1st April 2021. The new benchmark index has long term performance very similar to that of the former benchmark, but the Board believes that the new benchmark has the benefit of being more widely recognised by investors.

Gearing/Borrowing

The Company seeks to enhance investment returns for shareholders by borrowing money to buy more assets (‘gearing’). The Company’s gearing is discussed regularly by the Board and the Investment Managers, and the gearing level is reviewed by the Directors at each Board meeting.

The Company has a revolving credit facility of Yen 4.0 billion (with an option to increase available credit to Yen 6.0 billion) with Scotiabank. This facility has a maturity date of October 2022. The loan facility is on favourable and flexible terms, allowing the Company to repay the loan early if required, without any penalties.

This credit facility provides the Managers with the ability to gear tactically within the set guidelines. The Company’s investment policy permits gearing within a range of 10% net cash to 25% geared. However, the Board requires the Investment Managers to operate in the narrower range of 5% net cash to 15% geared, in normal market conditions. During the six months of the review period the Company’s gearing level ranged between 5.8% to 9.8%, ending the half year at 7.8%.

Auditor Review

The last formal exercise of audit tender was undertaken in 2014, when Grant Thornton was appointed. The Company’s year ended 31st March 2021 was the last of a five year tenure of Grant Thornton’s audit partner, Marcus Swales, who was overseeing the compilation of the Company’s accounts, and a new partner was expected to take over.

The Board took the view that this change provided an opportune moment to review the Company’s audit arrangements. The Board also felt that a review would give the Directors the chance to survey the market and ensure that the Company’s audit arrangements remain competitively priced, providing good value for shareholders, while also maintaining the same high quality of the statutory audits. To this end, the Board undertook a tender process for the 2022 statutory audit. Following a review of tender proposals from three firms, Johnston Carmichael LLP has been appointed as the Company’s new auditor. A letter has been sent to shareholders of the Company today pursuant to Section 520(2) of the Companies Act 2006. The letter is for information only and relates to the statutory statement received from Grant Thornton LLP in connection with its ceasing to be the Company’s auditor with effect from 9th December 2021.

Outlook

There is no doubt that the global recovery is broadening out and gathering momentum, as economic activity returns gradually, if sometimes hesitantly, to normal. The Board shares the Investment Managers’ confidence that the pandemic has triggered significant positive structural changes within Japan, whose economic and societal benefits will continue to resonate well into the future. The impetus the pandemic has given to Japan’s digitisation efforts is likely to be particularly positive for productivity over the medium term. Furthermore, Japan’s membership of the new regional trading bloc, the Regional Comprehensive Economic Partnership (RCEP), should increase its access to the region’s rapidly expanding economies. Japan’s smaller, more entrepreneurial and innovative companies are leading the way across a variety of sectors and should thrive in this environment, generating many exciting investment opportunities. The Board believes the Investment Managers’ focus on quality and growth, supported by JPMorgan’s extensive, global and Tokyo-based research resources, means the Company is ideally placed to capitalise on these opportunities, and to continue to deliver attractive returns and outperformance for shareholders over the longer term.

Alexa Henderson

Chairman 10th December 2021

INVESTMENT MANAGERS’ REPORT

Performance and market review

Over the six months to September 2021, the Company outperformed its benchmark, the MSCI Japan Small Cap Index (in GBP terms), by 2.3 percentage points, delivering a return of +7.2% on net asset value (‘NAV’) compared to the benchmark return of +4.9%. The Company’s performance also beat the broader TOPIX index, which returned +6.8% (in GBP terms) over the review period. The Company’s performance is also notably ahead of the benchmark over the longer term. It has outpaced the benchmark by an average of 7.8 percentage points per annum over three years, and by 6.3 percentage points per annum over five years.

During the review period, the market advanced in response to surging optimism about the economic outlook, as the vaccination rollout progressed and COVID infection rates showed clear signs of peaking. Japan’s state of emergency was lifted at the end of September. Japanese Prime Minister Yoshihide Suga announced his intention to step down and Fumio Kishida was elected as the new president of the ruling Liberal Democrat Party (LDP) at the end of September. He replaced Suga as Prime Minister in October, following the LDP’s victory at a general election. The Japanese yen weakened against the US dollar and sterling on expectations that both the US Federal Reserve and the Bank of England would begin raising interest rates to dampen inflation pressures. The yen ended the review period at 111 yen to the US dollar, and 150 yen to sterling and has weakened further since.

Spotlight on stocks and sectors

During the six months under review, both stock selection and sector allocation had positive impacts on performance.

The stocks that contributed most significantly to returns included Benefit One, LITALICO, and Money Forward. These companies are leaders in their respective fields and all have performed well thanks to improvements in their earnings prospects, which have been boosted by structural changes in Japan’s labour market and business practices.

• Benefit One provides fringe benefit services for enterprises of all sizes. Japan’s declining working population has resulted in a major shift in the employment market. Historically, the supply of labour was plentiful and companies had a tendency to overstaff. But now employers are experiencing staff shortages, and they are offering attractive employee benefits to retain staff. Benefit One’s services include hotel and restaurant bookings, gym memberships, and care services for children and the elderly. The company recently acquired its competitor, JTB Benefit Service, which will give Benefit One the dominant share of this market.

• LITALICO specialises in employment support services for people with disabilities. It is the leading company in this market. Diversity and inclusion issues are gaining prominence in Japan and companies are increasing their efforts to ensure their workplaces are more inclusive, regardless of their employees’ gender, age, nationality, or disabilities.

• Money Forward is Japan’s leading supplier of cloud based accounting software. This is a new market in Japan, with significant scope to expand. Many companies are still using packaged software, and cloud accounting software presently accounts for only around 20% of the market – lower than in other developed countries. However, as in many other sectors, the pandemic has encouraged companies to update and digitise their working practices.

At the stock level, negative contributors to relative performance over the review period included Miura Kogyo, which manufactures small gas boilers, Bengo4.com, which operates a legal search and consultation portal, and Kaizen Platform, which provides digital outsourcing services to marketing and advertising companies. However, despite their near-term setbacks, we believe these companies all possess competitive advantages that will ensure their continued growth over the long term, so we have maintained our holdings.

With respect to sector allocation, top contributors to relative performance included our overweight position in commercial and professional services, which have benefited from structural changes in the labour market, and our longstanding underweight position in banks which we have avoided, as the sector is overcrowded and there is little to distinguish the product offering of any one bank from that of its many competitors. The main detractor from performance at the sectoral level was an underweight in transportation which we have also avoided due to tougher competition in the industry. The portfolio’s modest gearing, which averaged 8.3% over the period, had a positive impact, by increasing the portfolio’s exposure to the rising market.

About our investment philosophy

The Company has a commitment to provide its shareholders with access to the innovative and fast-growing smaller companies at the core of the new Japanese economy. Our portfolio favours quality and growth businesses and we aim to invest in companies (other than Japan’s largest 200) that we believe can compound earnings growth over the long term, supported by sustainable competitive advantages and good management teams. In our view, the strong and durable market positioning of such businesses will allow them to substantially increase their intrinsic value over time. We are also attracted to companies willing to invest to enhance their growth potential. We generally avoid stocks that operate in the financial and real estate sectors, which are plagued by excess supply and undifferentiated product offerings.

Our focus on high quality names with growth potential means that the portfolio tends to enjoy a high active share and differs significantly from the benchmark. This provides a source for additional return, enhancing the Company’s scope to outperform. We believe it is important to take a long-term perspective, as excess returns take time to accumulate, especially when investing in smaller companies.

The Company is managed by a team of three, with an average of 15 years’ experience with JPMorgan Asset Management (JPMAM) and 20 years’ industry experience. We are supported by JPMorgan’s extensive research resources, located in several offices around the world. Our stock selection is based on fundamental analysis, which is informed by the in-depth, ‘on-the-ground’ knowledge and expertise of 29 Tokyo-based investment professionals. As such, they are ideally placed to identify interesting investment opportunities. The Japanese equity market is very under-researched and thus inaccurately valued by most investors, so our well-resourced local research team enjoys a significant advantage in discovering and exploiting the market’s information and valuation anomalies.

Japan’s smaller companies market offers many such opportunities, across diverse sectors with strong growth potential. Many of the constituent businesses operate internationally, as well as in the domestic market. Moreover, an increasing number of smaller firms have recently increased their focus on improving their return on equity and enhancing dividend yields.

In our view, a consistent investment approach is also key to successful long term investing. So, while the portfolio tends to struggle during ‘value’ rallies, when our bias towards quality and growth stocks slips out of favour with investors, we do not view this as a reason to alter our investment process or style. We remain focused on quality names with structural growth opportunities. The Company does not, however, operate under a ‘growth at any price’ strategy and we continue our efforts to ensure that we pay a fair price for each investment, based on our estimate of its five-year expected return.

To minimise exposure to unintended risks, we have constructed a well-balanced and diversified portfolio, that is invested in smaller companies across a wide range of sectors, including not only technology stocks providing software and hardware products, but also materials, chemicals, construction, machinery, retail and restaurant outlets and other consumer goods and services. We also use gearing to enhance the portfolio’s returns, but deploy it conservatively to avoid excessive exposure to downside market risk.

We believe that well-run companies, which exhibit behaviour which respects the environment and the interests of their shareholders, customers, employees and other stakeholders, are most likely to deliver sustainable, long-term returns. Such environmental, social and governance (‘ESG’) considerations are thus integral to our investment process and a key driver of our quest to generate financial returns. ESG factors influence our decisions both at the portfolio construction stage and thereafter, once companies are held in the portfolio, when ongoing engagement with managers can be effective in encouraging them to realise and maintain acceptable ESG standards. Our long-term holdings in Benefit One and Litalico (discussed above) are a couple of manifestations of the way in which ESG considerations influence our investment decisions, as both these companies are at the forefront of Japan’s efforts to improve employee well-being and workplace diversity.

Trends and themes

While our investment decisions are based on company-specific factors, several long-term structural trends and themes underlie our stock selection. These include:

• Changing demographics: Japan’s population is declining, and the elderly make up an increasingly large percentage of the country’s total population. This is a significant economic challenge for the Japanese government, for many reasons, including the associated contraction in Japan’s labour supply. However the government is committed to addressing these issues through digitisation and regulatory reforms. At the same time, this demographic shift is creating opportunities for innovative smaller firms working to improve the quality of life for older people, for example, by increasing their access to online banking and reducing the need for face-to-face medical appointments.

• Government efforts to digitise the economy and raise labour productivity: The Japanese government aims to accelerate the adoption of digitisation across the economy. To this end, it has established a digital agency to step up the pace of innovation, raise labour productivity, and digitise national and local government administrations, the education system, and healthcare services. Companies operating in all these sectors, either as suppliers or users of productivity-enhancing digital services, will benefit.

• Technological innovation: Japanese manufacturers are world class and the country is a leading global supplier of factory automation equipment, robots, electronics parts and materials. Demand for these products presents a myriad of investment opportunities for businesses specialising in niche markets for related products and services.

• De-carbonisation: Reducing carbon emissions is an essential part of the global fight to mitigate climate change. Japanese smaller companies have developed unique technologies to help meet this challenge in areas such as electric vehicle production and in solar and wind power plants, as well as other sources of renewable and clean energy. We are also continuing our search for other businesses well positioned to profit from the global push towards carbon neutrality.

• Enhanced corporate governance standards: Japanese companies are making concerted efforts to strengthen their governance standards, encouraged by a spate of government reforms. The number of independent external directors serving on company boards has increased, and corporate practices have improved; internal controls and disclosures have been enhanced and returns to shareholders have risen. However, there is still room for further improvement, and the market is likely to keep rewarding businesses that raise their governance standards. We maintain constructive dialogue with all the companies in our portfolio, to encourage them to maintain their efforts in this direction.

• Growing overseas demand: Many of Japan’s Asian neighbours are experiencing very rapid and dynamic economic growth, driven by the rise of their middle classes. Japanese luxury goods producers are experiencing rising demand for new customers in China, India, and other vibrant and increasingly prosperous Asian countries.

Positioning the portfolio for future success

Consistent with our search for companies set to benefit from these themes, and our ongoing focus on ESG considerations, recent acquisitions have included companies operating at the cutting edge of progress on de-carbonisation, digitisation and efforts to enhance employee wellbeing.

Yamato Kogyo, Tokai Carbon and Visional are three names which we have added to the portfolio during the past six months:

• Yamato Kogyo is a steel producer which uses electric arc furnaces, rather than conventional blast furnaces, in its manufacturing process. Electric arc furnaces emit only around one sixth to a quarter of the greenhouse gases (GHG) produced by conventional blast furnaces and Yamato Kogyo is one of the largest Japanese steelmakers using this technology. It also has joint venture operations and subsidiaries in the United States, Thailand, and other countries. The company is likely to see increased demand for its products as construction and manufacturing companies strive to reduce the carbon footprint of their steel inputs.

• Tokai Carbon is a play on the same theme. It is a leading global supplier of ultra-high quality graphite electrodes, which are a key component of electric arc furnaces. Demand for Tokai Carbon’s products is likely to escalate as steel companies phase out their use of conventional blast furnaces, in favour of more environmentally friendly electric arc furnaces.

• Visional provides education, training and recruitment services to businesses. Its BizReach service is a pioneer of direct recruiting in the professional employment market and it has recently launched a human capital management software product, called HRMOS. These two businesses have scope to grow over the long term as Japanese companies increase their focus on employee engagement and human capital management.

Three of our most significant divestments during the review period were Nippon Prologis REIT, Nohmi Bosai, and Fujitsu General. The Company’s investment guidelines prohibit investment in Japan’s top 100 securities and as Nippon Prologis REIT is approaching this threshold, so we closed our position, realising some sizeable profits. Nohmi Bosai and Fujitsu General have both seen sustained share price increases, making them less attractive from a valuation perspective, so we realised our profits on these positions, exiting them in favour of more interesting opportunities.

Over the review period, annualised portfolio turnover was around 25%, down slightly from the level of the previous financial year. The overall shape of the portfolio has not changed significantly and we maintain our bias towards quality and growth; the portfolio has a higher return on equity and higher growth in earnings per share than the overall market. The Company’s gearing level remained within the expected 8-10% range.

Outlook and strategy

COVID-19 and its aftermath continue to cast a shadow over the global economic outlook, with successive waves of the virus generating ongoing uncertainties, fresh rounds of restrictions, and delays to the resumption of international travel to many regions. However, despite these near-term obstacles to recovery, we believe there are good reasons to be optimistic about the longer term outlook. Vaccination programmes are gathering momentum, and global economic activity is recovering from the devastating effects of the pandemic. Furthermore, we expect the pandemic to leave significant and lasting positive changes in its wake, in Japan and elsewhere, including industry consolidation, supply chain diversification, and productivity gains from the more intensive use of digital technologies and flexible working practices.

Regardless of the economic backdrop, at any point in time, it is always important to focus on good quality businesses with leading market positions, strong cashflow generation, robust balance sheets and the potential for structural growth. Our search for such companies is aided by the fact that Japanese businesses typically have significantly large cash positions, and stronger balance sheets than their peers in other developed countries. In addition, the average valuations of Japanese companies remain reasonable, being lower than both historical averages and those of most other major markets. Furthermore, in sharp contrast to other developed economies, Japan’s smaller and more entrepreneurial companies are at the forefront of innovation in many fields, and set to prosper accordingly over the long term.

The Company’s access to JPMorgan’s extensive research resources on the ground in Tokyo means it is ideally placed to uncover exciting investment opportunities amongst smaller companies, and to capitalise on the long-term structural changes taking place in Japan, while weathering any short-term challenges posed by the pandemic, trade tensions or other transitory influences on market sentiment. We are therefore confident our investment approach will continue to deliver positive and sustained returns to our shareholders over the medium and long term.

Eiji Saito

Naohiro Ozawa

Michiko Sakai

Investment Managers 10th December 2021

INTERIM MANAGEMENT REPORT

The Company is required to make the following disclosures in its half year report.

Principal and Emerging Risks and Uncertainties

The principal and emerging risks and uncertainties faced by the Company have not changed and fall into the following broad categories: operational and cyber crime; investment performance and strategy; share price discount to net asset value; loss of investment team or investment manager; political and regulatory; financial; climate change; and, pandemic risk. Information on each of these areas is given in the Business Review within the Annual Report and Financial Statements for the year ended 31st March 2021.

Related Parties Transactions

During the first six months of the current financial year, no transactions with related parties have taken place which have materially affected the financial position or the performance of the Company during the period.

Going Concern

The Directors believe, having considered the Company’s investment objectives, risk management policies, capital management policies and procedures, nature of the portfolio and expenditure projections, that the Company has adequate resources, an appropriate financial structure and suitable management arrangements in place to continue in operational existence for the foreseeable future and, more specifically, that there are no material uncertainties pertaining to the Company that would prevent its ability to continue in such operational existence for at least 12 months from the date of the approval of this half yearly financial report. For these reasons, they consider that there is reasonable evidence to continue to adopt the going concern basis in preparing the financial statements.

Directors’ Responsibilities

The Board of Directors confirms that, to the best of its knowledge:

(i) the condensed set of financial statements contained within the half yearly financial report has been prepared in accordance with FRS 104 ‘Interim Financial Reporting’ and gives a true and fair view of the state of the affairs of the Company and of the assets, liabilities, financial position and net return of the Company as at 30th September 2021, as required by the UK Listing Authority Disclosure and Transparency Rule 4.2.4R; and

(ii) the interim management report includes a fair review of the information required by DTRs 4.2.7R and 4.2.8R of the UK Listing Authority Disclosure and Transparency Rules.

In order to provide these confirmations, and in preparing these financial statements, the Directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgements and accounting estimates that are reasonable and prudent;

• state whether applicable UK Accounting Standards have been followed, subject to any material departures disclosed and explained in the financial statements; and

• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company will continue in business;

and the Directors confirm that they have done so.

For and on behalf of the Board

Alexa Henderson

Chairman, JPMorgan Japan Small Cap Growth & Income 10th December 2021