JPMorgan Japan Small Cap Growth & Income (LON:JSGI) offers its investors a way to access the structural growth opportunities within Japan’s small- and mid-cap equity market. JSGI is run by a three-strong team based locally in Tokyo, who are in turn supported by a substantial team of 25 equity investment specialists. The team aim to capitalise on a number of trends which they believe are driving the modern Japanese economy, purchasing the highest-quality growth-focussed stocks that are able to capitalise on these opportunities. JSGI’s portfolio is also characterised by its high active share and low turnover.

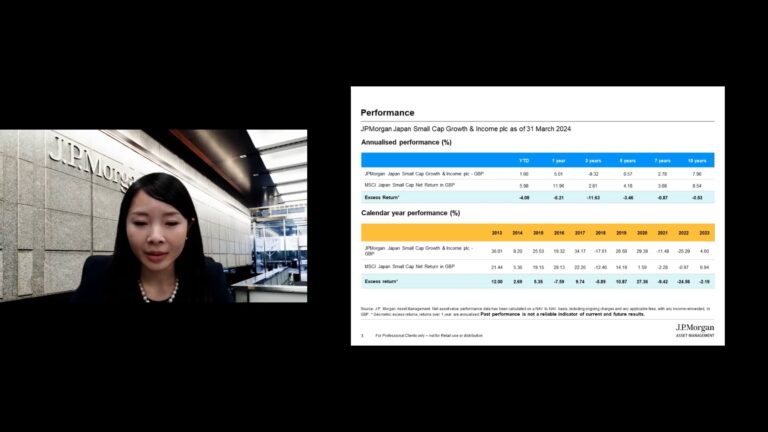

JSGI has been able to outperform its peers and benchmark, the MSCI Japan Small Cap Index, over the longer term. It has done this with an attractive risk–return profile, including lower volatility and downside capture than its peers. However, due to the headwinds impacting its quality growth style, it has underperformed over the last 12 months.

One of the most distinguishing features of JSGI is its income profile. JSGI currently has a policy of paying out 1% of its NAV each quarter as a dividend, which equates to a historical yield of 4.0%. This means it offers a high yield from a market that income investors are unlikely to have much exposure to, bringing diversification potential, as we highlight in the Dividend section. JSGI currently trades on a 8.4% discount which is narrower than its five-year average, reflecting the positive reception of its dividend policy and the long-term tailwinds supporting Japanese growth investing.

Kepler Trust Intelligence Analyst’s View

While we view JSGI as being an attractive proposition for any growth-minded investors wishing to access the structural trends underpinning Japan’s economy, we believe that JSGI’s dividend profile makes it a unique proposition. Generating an attractive level of income from Japanese equities is a challenge, given their historically low yields and the governance issues facing Japanese companies. Yet by being able to capitalise on its closed-ended structure, we believe that JSGI offers income investors a truly unique and attractive proposition. Not only does it offer an attractive yield, but it also offers access to an often-overlooked market with diversification benefits. Thanks to the team’s quality growth bias, it also offers an investment style with a strong structural growth story that income investors seldom have access to without having to sacrifice on yield.

Japanese growth stocks are facing near-term headwinds, which are reflected in JSGI’s 12-month performance as well as its current discount, which in our view could make an attractive entry point. Long-term investors able to ride out the current markets may find it possible to capitalise on a potential narrowing of JSGI’s future discount if we return to more supportive markets.

In our view Eiji Saito, Naohiro Ozawa and Michiko Sakai’s approach is conducive to long-term capital growth, thanks to Eiji’s stalwart commitment to capitalising on the trends of ‘new Japan’. However, if the current value stock rally continues JSGI may also continue to underperform, as its holdings are typically sold off during the early stages of an economic recovery.