")

")

")

")

")

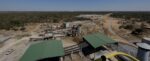

Firering increases Limeco stake to 41.7% after breakeven milestone

Firering has exercised the fourth tranche of its Limeco option, raising its stake to 41.7%, as production ramps up, costs improve and Limeco expands its customer base across Southern Africa.