Echo Energy plc (LON:ECHO), the Latin American focused upstream energy company, has announced the following Board changes. Stephen Birrell has been appointed as Chief Executive Officer (‘CEO’) of the Company with immediate effect. Stephen is highly experienced geoscientist who has worked in the upstream oil and gas and mining industry for over 35 years with a particular focus on gas developments across multiple jurisdictions with Britoil, BP and Elf and Sterling Resources, where he discovered and initiated the development of the Black Sea gas field complex, Ana/Doina in Romania. Stephen has a BSc Honours in Applied Geology and is a member of the Association of International

Echo Energy PLC (LON:ECHO) has announced its Interim Results for the period ended 30 June 2023. Chairman’s and Chief Executive Officer’s Statement In the 2022 Annual Report, released at the same time as this 2023 Interim Report, the following statement was made. “Echo Energy, similar to many companies in the oil and gas sector, faced exceptional challenges during recent years, with the global pandemic impacting all aspects of the Company’s operations and finances in Argentina. The Company emerged from the COVID-19 period (during which the assets were sub economic) with a large creditor position, 100%+ per annum inflation in Argentina and Argentine currency

Echo Energy Plc (LON:ECHO), the Latin American focused energy company, has announced that, further to the Heads of Terms announced on 9 May 2023, the Company has now signed binding transaction documents, subject to shareholder approval, on broadly the terms outlined in the Heads of Terms. The Board of the Company is requesting shareholder approval for the partial sale of its Santa Cruz Sur assets on the basis that it: · Addresses the Company’s near-term funding challenges by providing near term funding, enabling the Company to transfer to Buyers the significant in-country creditors which had built up during the COVID-19 period and providing

Echo Energy plc (LON:ECHO), the Latin American focused energy company, has announced the execution of a binding Term Sheet for a transaction, subject inter alia to shareholder approval, designed to provide much needed funding for the Company through the sale of 65% of the Company’s 70% of the current Working Interest in Santa Cruz Sur to Selva Maria Oil S.A. and Interoil Exploration and Production ASA for a cash consideration of up to £1.725M, an award of an option to purchase a producing Columbian portfolio and the issue of equity in Echo Energy PLC at 0.065 pence per share (a more than 100% premium

Echo Energy plc (LON:ECHO) CEO Martin Hull joins DirectorsTalk Interviews to discuss a commercial update regarding the Company’s gas sales from the producing Santa Cruz

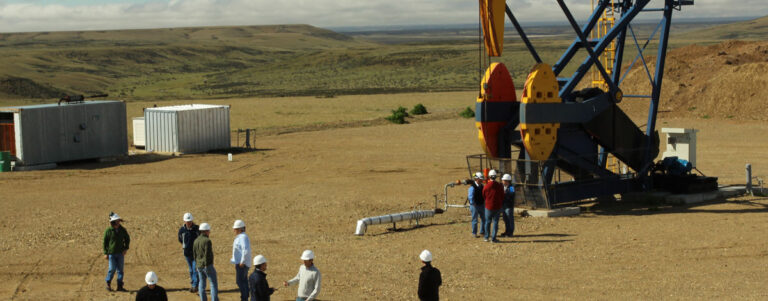

Echo Energy (LON:ECHO), the Latin American focused energy company, has provided a production update regarding its Santa Cruz Sur assets, onshore Argentina, for Q3 2022.

Echo Energy plc (LON:ECHO) CEO Martin Hull joins DirectorsTalk Interviews to discuss successfully raising £0.6 million in an oversubscribed placing. Martin shares his thoughts on

Echo Energy plc (LON:ECHO) CEO Martin Hull joins DirectorsTalk Interviews to discuss its latest production update and an agreement to increase production with its partners.

Echo Energy plc (LON:ECHO) Chief Executive Officer Martin Hull caught up with DirectorsTalk to discuss the new gas contracts, delivering on strategy, improved creditor situation,

Echo Energy plc (LON:ECHO) Chief Executive Officer Martin Hull caught up with DirectorsTalk to discuss result of the bondholder meeting, the key points of the

Echo Energy plc (LON:ECHO) Chief Executive Officer Martin Hull caught up with DirectorsTalk for an exclusive interview to discuss their latest production & operational update,

Echo Energy plc (LON:ECHO) Chief Executive Officer Martin Hull caught up with DirectorsTalk for an exclusive interview to discuss highlights from the interim results, restructuring

Echo Energy Plc (LON:ECHO), the Latin American focused energy company, has provided an operational update regarding its Santa Cruz Sur assets, onshore Argentina, for the