TEAM Asset Management’s global weekly market review for week commencing 27th November. TEAM Asset Management is a Jersey-based independent asset management company of AIM-listed parent, TEAM plc (LON:TEAM).

US equity markets recorded their fifth consecutive positive return on the week, capping a spectacular month for risk assets. The bellwether S&P large cap index advanced +8.9% in November, its 18th biggest monthly gain since 1950, whilst the Bloomberg US Aggregate Bond Index closed +4.5% higher for its best month since May 1985. Various sentiment surveys indicate that investor optimism is widespread and at elevated levels.

The genesis of the rally appears to be a rapid resetting of expectations with regards to the future path of monetary policy. Markets cheered positive inflation data, with the latest release of the US Federal Reserve’s preferred gauge for tracking inflation, the Personal Consumption Expenditures Price Index (‘PCE’), showing that consumer prices continued to rise at a slower pace in October (+3.0% annual rate, down from +3.4% in September).

The inflation data forms part of a growing body of evidence that cracks are, it would seem, finally appearing in the US economy. The government also reported last week that spending by U.S consumers, the primary growth engine of the economy, rose in October at an annual rate of +0.2%, the slowest pace in five months and a sharp slowdown from September’s +0.7% figure. October’s unemployment rate also edged up to 3.9%.

All taken, markets are now convinced that the US Federal Reserve will not raise interest rates again in this cycle and that aggressive rate cuts are imminent, beginning in the first quarter of 2024. A similar theme is playing out closer to home where the European Central Bank and the Bank of England are now expected to slash the benchmark interest rate by almost two percentage points and sixty basis points (0.6%) in 2024.

Turning to the earnings ‘scores on the doors’, S&P 500 index companies posted an average earnings gain of +4.7% over the same quarter a year earlier, according to FactSet data from the recently concluded earnings season. That result marked the first year-over-year earning increase since the third quarter of 2022.

In terms of results success, the performance variation between sectors was high. Communication services was the standout sector, with spectacular earnings growth of 42% going some way to justifying the eye-watering outperformance year-to-date from the Magnificent 7 (Apple, Amazon, Alphabet, Nvidia, Meta, Microsoft, and Tesla). Investors are betting that this handful of companies are best positioned to benefit from productivity gains generated by the artificial intelligence and robotics theme.

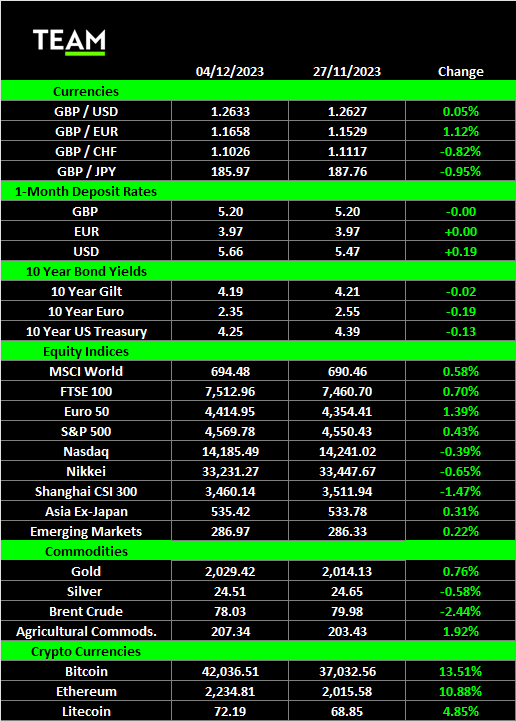

Finally, against a backdrop of slowing inflation, a potential peaking of interest rates, and a weakening dollar, gold has regained its allure, briefly touching new all-time highs of $2,100. In crypto currency world, Bitcoin surged past $40,000, hitting 2023 highs over the weekend on growing enthusiasm for an anticipated approval of a Bitcoin spot Exchange Traded Fund in the US. Despite soaring over 80% year to date, Bitcoin is still down c.40% from its all-time highs.

Looking to the week ahead, the US employment data has arguably taken the baton from inflation in being the most important data point to watch globally. Friday’s labour market report will show whether a recent slowdown in U.S jobs growth extended into November.