Boku Inc (LON:BOKU) Chief Executive Officer Jon Prideaux caught up with DirectorsTalk for an exclusive interview to discuss first half highlights, payments division, Mobile First Network, Identity and what we can expect in the coming months.

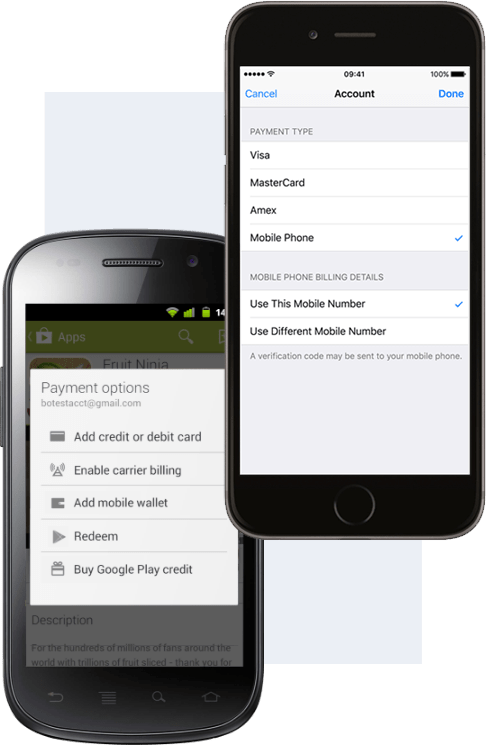

Boku is a mobile payments company that allows businesses to collect online payments through both carrier billing and mobile wallets. Now, today the company announced its interim results for the six months ended 30 June 2021 and joining me to discuss those results is Boku CEO, Jon Prideaux.

Q1: Jon, as mentioned, you’ve released your half year results this morning, another period of strong growth. Can you just talk us through the highlights of the first half?

A1: Operationally, both divisions performed well. We had lots of launches across all of our business lines, DCB bundling on wallets with essentially most of our major merchants, companies like Apple, Google, Netflix, and Spotify, and so on. The other main operational benefit we had was was launching our Mobile First Network.

Well, those two things led us to having a really great revenue and EBITDA performance. Revenue that we posted in the half was up by 38% to $34.2 million, that was flattened little bit by the acquisition of Fortumo that we did, but even accounting for that, the underlying organic revenue growth was 21%. EBITDA did even better because there’s strong operational gearing in the business and that led to an EBITDA growth at the group level up 61% to $10.3 million so a pretty satisfactory set of results, I think.

Q2: Can you just tell us a bit more about how the payments division has progressed over the first half of 2021? And also explain more about what you’re calling M1ST, or Mobile First Network, and how they all drive future growth?

A2: Historically, the company has allowed people to buy things and charge it to their phone bills and we grew to be really the largest player of that type, serving digital entertainment companies, a fact that I mentioned earlier.

What we figured out is obviously having that incumbency gives us the ability to go and support other payment methods as well and so, as you mentioned in your own introduction, we’re now also strongly supporting new payment methods like mobile wallets. The really exciting thing about that is the fact that where it’s direct carrier billing, they’re buying stuff and charging it to your phone bill, is probably limited to about 15% of what someone is going to spend on a merchant’s website.

With wallets, you can get up to 50% or 60%, much much bigger numbers and so we launched our M1ST network, or Mobile First Network, which brings together something like 330 different payment types, mostly direct carrier billing, but also a couple of dozen wallets and other real time payment mechanisms as well.

Many of our largest merchants have now taken this, alongside other merchants taking the programme, and all of these things helped us to push growth in the payments division up to about 40% to $30.7 million, that was an organic growth of about 20% in that business. EBITDA there went up to about $11 million.

Of course, we’re operating off this strong base of having had the Fortumo acquisition, that really cemented our position of leadership in DCB, really gives us a chance to become a mainstream payment mechanism. I think now we correctly need to be seen in that peer group of other specialised payment processes rather than working on local payment methods in general, rather than just being a one trick pony with direct carrier billing.

Q3: Just moving on to the identity division. How has that side of the business been doing?

A3: Much improved. I think if you look at 2020, we had somewhat of a fallow year, driven really by some supply interruption in the US, we’re reconnected in the US and most pleasingly, we’ve been making some real strides in our international business. The revenues there were up 30% at $3.5 million, losses reduced to just a fraction under $1 million dollars and mostly that was driven by a strong organic performance in the international division.

We had a new business in Indonesia, new connections launched in places like Italy and Spain and so that’s a pretty pleasing turnaround from the identity division, really following through on the strategy that we were trying to execute ever since we got into this business.

Q4: And just to wrap up, can you summarise what we can expect from Boku in the rest of the year and perhaps into 2022?

A4: It’s a bit boring, but I guess we’re expecting another record year, clearly revenue is growing strongly.

The most important thing that we’re trying to do in terms of executing is trying to continue this transition, this Mobile First, this M1ST strategy, of trying to launch ever more payment types, to really help our customers connect to those Mobile First Consumers, predominantly in Asia, but also Latin America and Africa, and we really expect to see that develop.

This year’s results, we’re confident in our ability to meet the markets and our expectations and we look forward to a bright future in the medium term as well.