Boku Inc (LON:BOKU), a leading global mobile payment and mobile identity company, has announced the following unaudited interim results for the six months ended 30th June 2020.

Highlights

Group

· Group Adjusted EBITDA* for H1 2020 of $6.4 million is 84% higher than H1 2019 (H1 2019: $3.5 million adjusted for a one time revenue item**. H1 2019 reported Adjusted EBITDA $4.3 million)

· Group Revenues for H1 2020 increased to $24.7 million (H1 2019 $22.7 million**, excluding the impact of a non-recurring payments item: $23.5 million reported)

o Payments – Underlying Payments revenue** growth has been strong at over 13.7% to $22.0 million

o Identity revenue of $2.7 million impacted by coronavirus though with minimal effect on Group Adjusted EBITDA

· Adjusted operating expenditure*** of $16.0 million for H1 2020 is in line than the same period last year (H1 2019: $16.3 million) as coronavirus reduced marketing/events costs and T&E across the Group

· Operating Profit for H1 2020 of $0.2m compared to an operating loss of $2.3 million for the same period in 2019

· Acquisition of DCB payments company Fortumo Holdings Inc (“Fortumo”) completed on 1 July consolidating Boku’s dominant position in the global Direct Carrier Billing (“DCB”) market

· Group cash of $80.7 million at 30 June 2020 which included $44.5 million of cash held to pay for the acquisition of Fortumo on 1 July 2020. Excluding this cash, Group cash balance were $36.2 million inclusive of $0.8 million of restricted cash (31 December 2019: $35.6 million including $0.9 million of restricted cash). To part-fund the Fortumo acquisition a new $20.0m debt facility was taken out in June and was fully drawn down at 30 June 2020. The balance of the acquisition funding was from a successful placing in June at 85p per share

· The average daily cash balance – a measure which smooths out the effect of carrier and merchant payments, was $25.7 million in June 2020 (December 2019: $22.4 million)

Payments division

· Underlying Payments revenues** increased by 13.7% to $22.0 million (H1 2019 $19.4 million , excluding the impact of a non-recurring item, $20.2 million reported) as Boku Payments benefited from the coronavirus pandemic particularly in April and May 2020.

· Payments Adjusted EBITDA* increased by 45% to $8.4 million (H1 2019 $5.8 million** excluding the impact of a non-recurring item. $6.6 million reported)

· Total Payment Volume (“TPV”)**** of $3.1 billion in H1 2020, 36% up on H1 2019 ($2.3 billion)

· 10.8 million new users made their first ever Boku transaction during the first half of the year, 19% up on the prior year, driven by increased adoption during the coronavirus lockdowns

· 20.3 million Monthly Active Users (“MAU”) of the Boku platform in June 2020 (June 2019: 15.3 million), a 33% increase

· Carrier billing launches in H1 2020 with Google, Netflix, Sony, Spotify and Tencent

· Good progress with eWallets with seven mobile wallets now live including Grabpay, GoPay and Dana and further contracts signed

Identity division

· Identity revenues of $2.7 million (H1 2019: $3.4 million). Revenues and new sales were impacted by coronavirus, though with minimal impact on expected Adjusted EBITDA

· Identity Adjusted EBITDA loss reduced to $2.0 million (H1 2019 $2.3 million loss)

· Good progress on building out international carrier supply – now live with more than 200 carriers in 60 countries. Contract wins including LexisNexis and FIS (owners of Worldpay) with merchants now live and generating revenues in five countries.

* Adjusted EBITDA (Earnings before interest, taxation, depreciation and amortization): Adjusted for stock option expenses, Forex gains/losses and Exceptional items. Underlying Group Adjusted EBITDA is Adjusted EBITDA less the $790k one time item mentioned in item **

** 2019 H1 revenue included $790k of one off revenues relating to a contractual change that accelerated revenue recognition of a large contract. This increased H1 2019 Adjusted EBITDA by the same amount

*** Adjusted operating expenditure is Gross Profit less Adjusted EBITDA

**** TPV is the US$ value of transactions processed by the Boku platform

Jon Prideaux, Boku’s CEO, commented:

“Boku’s core business of Direct Carrier Billing is in rude health. The Company has seen a boost in the adoption of digital services during the pandemic and has proved its ability to execute even as the majority of the Company are working from home. With this foundation, enhanced by a contribution from Fortumo, supporting our investment in Identity and a strong pipeline of customers for our Local Payment Method offer, including eWallets, I remain confident that full year Group Revenue and Adjusted EBITDA* performance will be at least in line with current market expectations.”

Chief Executive Officer’s Report

Simplicity: it’s worth paying for

Charlie Mingus the American jazz musician once said, “Making the simple complicated is commonplace; making the complicated simple, awesomely simple, that’s creativity.”

Boku’s customers, global companies like Apple, Sony, Spotify and Netflix don’t want to deal with 200+ different connections to mobile network operators (“MNOs”) they need someone to make the complicated simple. And that someone is Boku. We have done the hard work of building direct connections to most of the world’s big telcos and can thus provide a single, simple interface for them to implement. Connect once – reach the world. That aggregation unlocks the value latent in the MNOs of the world. By aggregation we have created value.

But it doesn’t stop there: in this new mobile world the way that people pay is also changing. We have also simplified the payment process. In the past, in the PC era, payment was a distinct step. You clicked to put things in your shopping basket and then clicked to checkout selecting your payment method, which could differ from transaction to transaction. Checkout was a fairly complex process. It was Amazon who introduced a 1-Click checkout and things have been taken further for mobile commerce.

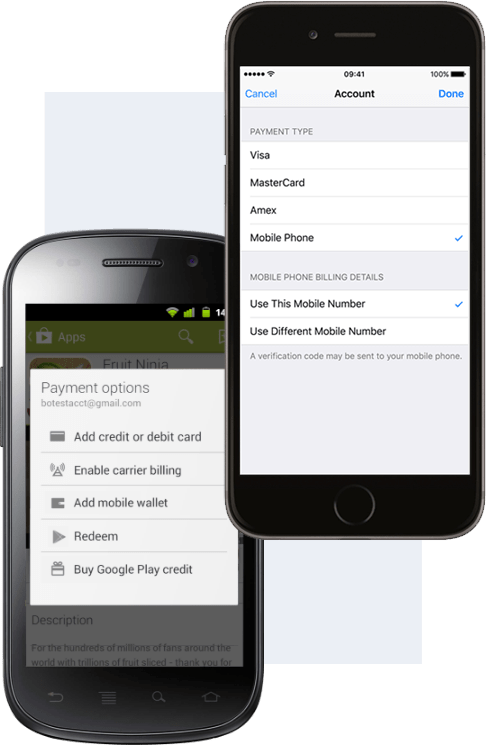

It is complex and fiddly to enter card details on a glass screen. It adds friction to the payment process. Friction that leads to fewer transactions, to more abandoned baskets. The simplest way of dealing with this friction is to eliminate the payment step altogether. To make payment a by-product of interacting with the app, to indicate the transaction or service you require and for payment to happen invisibly in the background. For this to happen you need register, to store a payment method on file.

Boku has made that awesomely simple: because the phone company knows your phone number without having to ask, it’s a simple as tapping once on the screen to put future charges through to your phone bill.

This philosophy has helped Boku’s core business of Direct Carrier Billing (“DCB”) to grow. Total Payment Volume (“TPV”) of $3.1 billion in the first half of 2020 was a 36% increase compared with the same period in 2019. Other companies have suffered through the pandemic. Not Boku. For us, adoption was accelerated as more people spent more time at home due to the coronavirus lockdowns and discovered digital entertainment. Nearly 11 million new users (+19% on H1 2019) made their first Boku transaction and experienced that simplicity for the first time, growing monthly active users in the month of June 2020 alone to more than 20 million.

Revenues in Payments grew by 13.7% (adjusting for a non-recurring item) and Adjusted EBITDA by 45% reflecting the high operating leverage implicit in Boku’s platform business.

Boku is now by some distance the leading player in the DCB industry, with strong volume growth, increasing revenue and operating leverage driving increases in Adjusted EBITDA. The acquisition of Fortumo on 1 July 2020 for an enterprise value of $41 million further cemented our position in this sector.

Business doesn’t travel in straight lines

Business doesn’t go in straight lines; it rises and falls in S-curves. The job of the CEO is not only to grow his business through a single S-curve, but to be laying the foundations for future growth by investing to find new S-curves to climb.

Boku has established itself as the leading Direct Carrier Billing company in the world. We’re processing transactions at a run rate of $7bn annually. Apple, Google, Sony, Microsoft, Spotify, and Netflix all use our services. We have grown revenues from $17 million in 2016 to more than $50 million in 2019. We will continue to grow as we roll out our merchants into new geographies.

Investors appreciate this growth. But we are not going to rest on our laurels, we’re investing to find new S-curves to climb.

DCB payments are mostly confined to digital commerce and, whilst this is not a small market, it is still only a fraction of global mobile commerce. DCB payments are strong in Europe, Asia and the Middle East. Growth in Latin America is picking up, but mainland China and North America are areas where for a combination of regulatory and commercial reasons, it’s not able to achieve traction. Boku aspires to enhance every mobile interaction: digital and physical in all parts of the world.

Boku’s merchant base and carrier network can be repurposed to new objectives. Rather than just allowing digital merchants to acquire new customers we can also help simplify mobile commerce for merchants in other verticals and re-use the skills developed to enable charges to be put through to phone bills also to support a whole range of Local Payment Methods (“LPM”), not just carrier billing.

One such Local Payment Method is eWallets. They’re the way that people, especially in Asia are starting to pay and Boku is now live and processing transactions with nine eWallets in seven countries. Mainstream Console and Digital Streaming Music merchants use Boku’s technology to reach eWallets in Indonesia and Korea. This expansion from DCB to LPM offers the chance of substantial returns. The same skills, platform and people can be repurposed to integrate LPMs at minimal additional cost to Boku giving powerful operating leverage. Volumes are currently modest, but will grow over the coming years to become a significant profit driver for the Group.

We’re also helping merchants to simplify the business of verifying phone numbers through our Identity business – heretofore a fiddly business involving text messages and one time codes. We can check the ownership of phones and detect account takeovers, one of the curses of our modern connected world. Boku Identity has made great strides in growing its network in 2020, but this is not yet reflected in the revenue numbers. Whilst DCB benefited from more people staying at home, Identity services, more dependent on people being out and about, suffered. Volumes and revenues on our existing customers were impacted, and new revenues in new geographies have not yet risen to compensate. First half revenues at $2.7 million were lower than the same period last year. Despite this, targeted investment and strict expense control delivered reduced Adjusted EBITDA* losses to $2.0 million in the first half (2019: $2.3 million).

We are building the world’s largest carrier identity network. The forward-looking indicators for the division are strong. The international supply network now extends to more than 200 carriers in 57 countries. Large customers are interested in the service and moving through the pipeline. Recent successes include LexisNexis and FIS, the owner of Worldpay.

Gradually then suddenly. eWallets and Identity are new businesses travelling the lower reaches of their S curves, but in time, will power our growth into the future.

Taken together the established business of DCB and the emerging Local Payment Method and Identity businesses have delivered growth: Group Revenues increased to $24.7 million and underlying Group Adjusted EBITDA* grew by 84% to $6.4 million . We are also pleased to be able to report a small operating profit for the period of $0.2 million.

Current Trading and Outlook

Boku’s core business of Direct Carrier Billing is in rude health. The company has seen a boost in the adoption of digital services during the pandemic and has proved its ability to execute even as the majority of the company are working from home. With this foundation, enhanced by a contribution from Fortumo, supporting our investment in Identity and a strong pipeline of customers for our Local Payment Method offer, including eWallets, I remain confident that full year Group Revenue and Adjusted EBITDA* performance will be at least in line with current market expectations.

Jon Prideaux

Chief Executive Officer

15 September 2020

Chief Financial Officer’s Report

The first half of 2020 was challenging for many companies due to the global coronavirus pandemic. The effect on Boku was positive in Payments, but less so in Identity.

Our Payments division benefited as international digital merchants like Apple, Netflix, Sony and Spotify benefited from an increase in demand for home entertainment and as a result this division performed strongly in H1. Good revenue growth to $22.0 million and lower than expected costs as the pandemic restricted travel, led to enhanced Adjusted EBITDA for the period. We also successfully completed a $25.0 million fundraise from existing investors in June to partly finance the acquisition of DCB company, Fortumo Holdings Inc (“Fortumo”) which was announced on 17 June 2020 and completed on 1 July 2020, and which consolidated Boku’s leading position in the global DCB market.

The impact on Boku’s Identity division was less positive. Revenues from some existing merchants – for example taxi services – reduced as their businesses were affected and new sales understandably slowed. However, headcount cost measures and Covid19 related savings in travel and marketing/events meant that Identity Adjusted EBITDA for H1 2020 was in line with expectations at a reduced loss of $2.0 million (2019: $2.3 million loss) on lower revenues of $2.7 million (2019: $3.4 million). Good progress was made on Identity supply during the period.

As a result, underlying Group Adjusted EBITDA of $6.4 million* was 50% higher than H1 2019 (H1 2019: reported $4.3 million). When adjusted for a one time revenue item** in H1 2019, the underlying like for like increase in H1 2020 is 84%, with Payments delivering $8.4 million of Adjusted EBITDA in the first half, partly offset by an Identity Adjusted EBITDA loss of $2.0million.

Financial review – Strong Adjusted EBITDA growth driven by Payments division performance

Group Income Statement to Adjusted EBITDA

We are pleased to report an 84% increase in Group Adjusted EBITDA to $6.4 million for the first half of 2020, (H1 2019: $3.5 million adjusted for a one time revenue item**. Reported $4.3 million), with Payments Adjusted EBITDA of $8.4 million up 45% on H1 2019 (H1 2019: $5.8 million**, $6.6 million reported) being offset by a reduced $2.0 million Adjusted EBITDA loss in Identity, (H1 2019: $2.3 million loss).

Group revenues for H1 2020 increased 9% to $24.7 million on an underlying basis (H1 2019 $22.7 million**, excluding the impact of a non-recurring payments item: $23.5 million reported). Coronavirus related lockdowns positively impacted the Payments division revenue which increased by over 13.7%** to $22.0 million while Identity revenues were negatively impacted and reduced slightly to $2.7 million.

Adjusted operating expenditure*** of $16.0 million for H1 2020 is in line than the same period last year (H1 2019: $16.3 million) as coronavirus materially reduced marketing/events costs in the Identity division and reduced travel and expenditure across the Group which we expect to continue in H2 however these costs are likely to return to normal levels next year. Payroll costs increased slightly due to planned annual pay rises and the Payments division invested in additional sales resource. However, Identity payroll costs were lower than in H1 2019 as the business refined its cost base.

$1.0 million of development expenditure was capitalised in H1 2020 reflecting the work undertaken to integrate and enhance the Boku Identity and Payments platform (2019: $0.7 million).

Boku Payments

Underlying Payments revenues** increased by 13.7% to $22.0 million (H1 2019 $19.4 million**, excluding the impact of a non-recurring item, $20.2 million reported) as Total Payment Volume (“TPV”)**** increased by 36% to $3.1 billion (H1 2019: $2.3 billion). Gross margin improved in the period as we received payment for previously provided for bad debts which increased margin by $211k.

Underlying Payments Adjusted EBITDA increased 45% to $8.4 million (H1 2019: $5.8 million**)

10.8 million New Users made their first ever Boku transaction during the first half of the year, 19% up on the prior year, driven by increased adoption during the coronavirus lockdowns. Monthly Active Users (“MAU”) of the Boku platform in June 2020 increased by 33% to 20.3 million (June 2019: 15.3 million).

Carrier billing launches were largely unaffected by Covid-19 and we launched multiple carriers worldwide in H1 2020 with major merchants such as Google, Netflix, Sony, Spotify and Tencent.

Average weighted take rates for Payments were in line with expectations at 0.7%. Boku’s transaction merchants, which have a lower take rate, continued to grow more quickly than its settlement merchants (where Boku provides a full cash collection service) where we charge a higher take rate. Take rates in both divisions were stable so the mix effect of more volume through our transaction merchants accounts for the small decline in blended take rates. Since IPO, Boku has not reduced its rates to any of its merchants nor has it lost a material merchant.

Good progress was made with integrations with eWallets, which is an entirely new market for Boku Payments, which it can access at minimal cost, with nine mobile wallets now live including Grabpay, GoPay and Dana and further contracts signed.

Acquisition of Fortumo

Boku completed the acquisition of DCB payments company Fortumo on 1 July for a maximum enterprise value of $41.0 million ($5.4 million of the consideration subject to meeting first year earnout targets) consolidating Boku’s leading position in the global DCB payments market. Fortumo primarily focuses on providing mobile payment solutions to over 400 small-to-medium sized enterprises, but also services larger merchants including Google, Amazon and Tencent. In 2019, Fortumo generated revenues of $7.2 million and Adjusted EBITDA of $2.3 million.

Boku Identity

Boku Identity revenues were impacted by the US carrier supply issue that occurred in late 2019 and by Covid-19 restrictions, which impacted both existing merchant revenues and new Identity sales. Revenues in the first half were $2.7 million (H1 2019: $3.4 million). Adjusted operating expenditure was lower than H1 2019 due to cost savings in headcount, reduced travel and marketing spend due to the pandemic, delivering a reduced Adjusted EBITDA loss of $2.0 million, (2019: $2.3 million Adjusted EBITDA loss).

Boku Identity made good progress on building out international carrier supply in H1 2020 and is now live with more than 200 carriers in 57 countries. Merchants are now live and generating revenues in five countries and Boku Identity saw a number of contract wins including with LexisNexis and FIS (owners of Worldpay).

Group Operating Profit

Group Operating Profit for H1 2020 improved by $2.5 million to $0.2 million compared to an operating loss of $2.3 million for the same period in 2019. This can be broken down as follows:

· Foreign Exchange movements resulted in a small gain of $0.1 million (H1 2019: $0.2 million gain)

· Stock Option Expenses – stock option expenses reduced to $3.0 million from $4.2 million in H1 2019 as Boku issued fewer Restricted Stock Units (“RSUs”) to staff in the period and during 2019 when compared to 2018. We expect this trend to continue going forward and that the annual charge for Stock Option Expenses will fall. Boku has issued either RSUs or share options to all staff annually. RSU and stock option charges are spread over three and four years respectively from the date of grant based on the Black Scholes method

· Exceptional Items of $0.9 million (2019: $0.3 million) related to acquisition costs incurred up to 30 June 2020 in relation to the acquisition of Fortumo which completed on 1 July 2020. Exceptional Items in H1 2019 related to the closure of our Italian entity and transaction costs relating to the Danal acquisition in January 2019

· Net financing expenses were reduced to $164k in 2020 (2019: $224k) which related to interest on right-of-use assets in particular office leases. There were no other interest payments as the Group had no borrowings until the loan to finance the Fortumo acquisition which was taken out on 30 June 2020

· The Group generated $6.0 million of cash from operations during H1 2020, prior to movements in working capital. (H1 2019: $2.8 million. This has been driven primarily by the improvement in Adjusted EBITDA

Balance Sheet and Cashflow

· Group cash balances were $80.7 million at 30 June 2020 which included $44.5 million of cash held to pay for the acquisition of Fortumo on 1 July 2020. Excluding this cash, the balances were $36.2 million (31 December 2019: $35.6 million). Included in this cash were restricted cash balances of $0.8 million

· To part finance the acquisition of Fortumo which completed on 1 July, Boku took on a debt facility of USD $20.0 million with Citibank in June which was fully drawn at 30 June 2020. This facility was split:

o $10m term loan repayable over 4 years; and

o $10m Revolving Credit Facility (“RCF”, “Revolver”) available to be drawn down in Euro, GBP or US$. Boku intends to use its surplus cash balances (see average daily cash balance point below) to partially offset the RCF balance during the monthly cycle and thereby reduce interest payments.

· The balance of financing was by way of a placing at 85p per share in June raising net proceeds of $24.1 million primarily from existing shareholders

· The average daily cash balance – a measure which smooths out the effect of carrier and merchant payments, was $25.7 million in June 2020 (December 2019: $22.4 million)

· We assessed our goodwill and intangibles for impairment and deemed that no impairment exists at 30 June 2020.

Principal Risks and Uncertainties

The principal risks and uncertainties facing the Group remain broadly consistent with the Principal Risks and Uncertainties reported in Boku’s 2019 Annual Report. Since the 2019 Annual Report, the Board have been monitoring and mitigating the effects of the following international events on the Group’s business:

Covid-19

In March 2020, the World Health Organisation declared a global pandemic due to the Covid-19 virus that has spread across the globe, causing different governments and countries to enforce restrictions on people movements, a stop to international travel, and other precautionary measures. This has had a widespread impact economically and a number of industries have been heavily impacted. This has resulted in impacts on certain industries and a more general need to consider whether budgets and targets previously set are realistic in light of these events.

As described above, the Covid-19 pandemic has impacted our business, both positively and negatively. The Board believes that the business is well positioned to be able to navigate through the impact of Covid-19 due to the positive impact of Covid-19 on its main Payments businesses, its dominant position in the niche Direct Carrier Billing market, its strong balance sheet and strong cash position.

Brexit

The United Kingdom (‘UK’) formally left the European Union (‘EU’) on 31 January 2020. The period of time from when the UK voted to exit the EU on 23 June 2016 and the formal process initiated by the UK government to withdraw from the EU, or Brexit, created volatility in the global financial markets. The UK is now in a transition period, being an intermediary arrangement covering matters like trade and border arrangements, citizens’ rights and jurisdiction on matters including dispute resolution, taking account of The EU (Withdrawal Agreement) Act 2020, which ratified the Withdrawal Agreement, as agreed between the UK and the EU. The transition period is currently due to end on 31 December 2020 and ahead of this date, negotiations are ongoing to determine and conclude a formal agreement between the UK and EU on the aforementioned matters.

Boku is not materially impacted by Britain’s withdrawal from the EU. Our business is growing fastest in Asia and already traded in a Europe of nations pre-Brexit. An immaterial amount of revenue is derived from EU passporting of our e-money licence.

Looking Ahead

The Covid-19 pandemic had a positive impact on our Payments division in H1 2020 increasing transaction volumes and revenues particularly in April and May, but also reducing our operating expenses as travel and entertainment costs reduced significantly – both of which improved Payments Adjusted EBITDA. Whilst most launches have proceeded as expected, a few have been pushed back. While the peak of the pandemic uplift has passed as full lockdown has ended in many countries, we have seen a continuing benefit from the accelerated adoption of subscription services, which is encouraging for H2 2020.

Boku’s Identity division was more adversely impacted by Covid-19 with volumes from existing merchants reduced as their businesses slowed and a slowdown in new sales as face to face meetings were not possible. However careful cost management and a continued build out of our Identity supply both directly and through partners means that progress was made and the Identity division is expected to show revenue growth and further reduced losses in 2021 as it moves towards cash breakeven.

While Identity remains a work in progress, on the Payments side the market consolidation from the Fortumo acquisition plus the substantial opportunity that eWallets present, allied to significant operational leverage that comes from our platform means we are confident for the future.

Keith Butcher

Chief Financial Officer

15 September 2020