- For the 2023 financial year, ending 31/10/2023, BRSA’s NAV and share price total return were -5.6% and -8.1% respectively, compared to a total return of -5.0% for the reference index, the Russell 1000 Value Index. Over the same period, the S&P 500 Index total return was 4.5% (all returns in sterling terms).

- The S&P 500’s performance was driven by a small number of mega-cap technology stocks, many of which do not have high dividend yields, benefiting from investor enthusiasm for new artificial intelligence technologies, which resulting in extremely strong share price performances.

- One of these stocks, Meta, briefly entered BRSA’s reference index but the managers chose not to own it first because it has no historical record of paying a dividend and second because its ESG scores are poor. Not owning this stock was one of the main factors behind the underperformance of the reference index. Increased scrutiny of ESG funds in certain US states also made for a challenging environment. It was also a generally challenging environment for value stocks, and the team estimates that the reference index is at one of its largest price to earnings discounts to the wider market in the last ten years.

- BRSA’s revenue earnings per share was 3.67p (2022: 3.84p), a decrease of 4.4%. Four quarterly interim dividends totalling 8.0p were paid (2022: 8.0p), equivalent to a 4.6% yield. The same policy and dividend amount will be in place for 2024, with dividends funded from current revenues and distributable reserves.

- The trust achieved a superior ESG score versus its reference index, as measured by MSCI, with an overall rating of AA, as well as a lower carbon emissions intensity than the same index. The FCA introduced its Sustainable Disclosure Requirements (SDR) in 2023, which differ from the EU equivalents that the trust currently complies with, and the board and manager are considering the implications of these and any changes that may be needed in order to comply, with a deadline for compliance of 2 December 2024.

- Over the financial year BRSA traded at an average discount of 6.0%, and the board repurchased 240,000 shares at an average discount of 9.1%. A further c. 780,000 shares were purchased post year end up to the beginning of February, with all shares held in treasury. Renewed authority to repurchase shares will be put to shareholders at the forthcoming AGM.

- Alice Ryder, Chair, said “Against a background of macroeconomic uncertainty and market volatility, our portfolio managers are of the view that an active approach to investing is likely to carry greater rewards. Additionally, our portfolio managers believe quality stocks with higher profitability, stronger balance sheets and stable earnings growth should outperform in an environment of persistent investor concerns over a mild recession in the US and other major developed economies. These are the fundamentals that our portfolio managers continue to favour within your company’s portfolio.”

Kepler View

Whereas BlackRock Sustainable American Income Trust’s reference index is, by Tony and the team’s calculation, at a P/E discount to the market rarely seen in the last ten years, they also note that the S&P 500 is above its twenty-year average, at over 19x compared to the average of c. 16.4x. The team also sees some warning signs in the economic data which means they believe the US economy is in a ‘late cycle’ phase, where there is a risk of a slowing economy and even a recession. They cite the low unemployment figures, rapid tightening by the Fed, negative money supply growth, an inverted yield curve together with consumers spending more and saving less as factors causing them concern. As a result of both valuation gaps and their economic concerns, they believe that valuation and stock picking will be key, and they are maintaining their focus on quality and valuation.

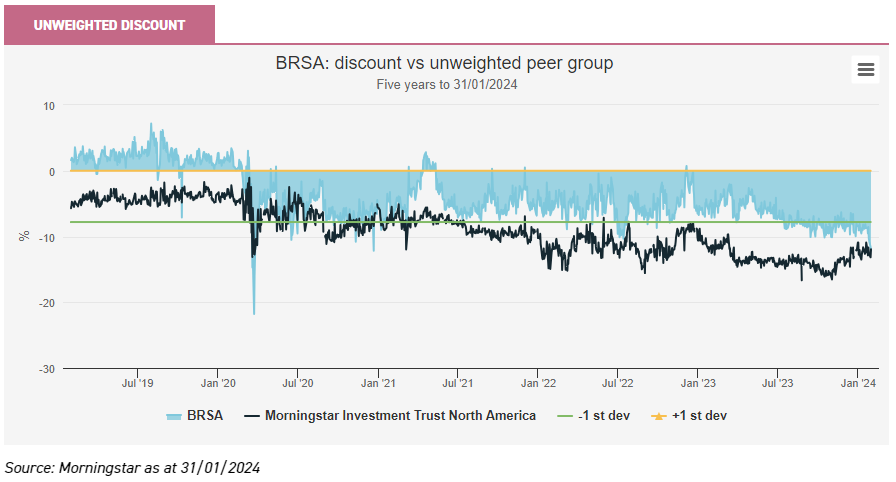

Like many investment trusts BlackRock Sustainable American Income (BRSA) has not been immune to discount widening. The chart below shows BRSA’s discount against its AIC North America peer group average. Given the outsize weight of Pershing Square Holdings (PSH) in this peer group at over 70% of the total, we have used an unweighted average, which gives a fairer picture of where BRSA stands. An average over the last 12 months of c. 7% has crept out to c. 12%, which is in line with the peer group. While the board has not committed to a specific target discount, buy backs have been used frequently in the last three months in particular as the discount widened towards the peer group average.

One of the reasons BRSA has generally traded at a narrower discount than its peer group is its dividend policy, and the board reaffirmed the dividend rate of 8 pence per share for the current financial year, using a mixture of revenue and reserves. BRSA, in contrast to many trusts that pay dividends using distributable reserves, has not historically adjusted its dividend in parallel with a rising and falling net asset value, but has maintained a constant dividend, giving investors greater certainty over their income.

Investors worried about stretched valuations in US equities, and about the very narrow range of stocks that have driven performance in the last year, could find BRSA an interesting alternative regardless of their ESG requirements. If their worries about a slowing economy prove well-founded, we think the defensively positioned portfolio could perform well as valuation reasserts itself as an important metric.

You can read more about BRSA by Kepler here